Practical Strategies for Managing Personal Debts Effectively

Learn practical strategies for managing personal debts, improving financial health, and regaining control of your finances. Follow these actionable tips to reduce and eliminate debt.

Welcome to the Wealth BluePrint.

Here, you’ll get practical strategies, smart financial insights, and business tips to grow and thrive.

Stay tuned

How to Manage Your Personal Debts

Table of Contents

Understanding Personal Debt

Assessing Your Financial Situation

Creating a Budget

Prioritizing Debt Payments

Exploring Debt Consolidation Options

Negotiating with Creditors

Avoiding New Debts

Building an Emergency Fund

Monitoring Your Progress

Seeking Professional Help

Understanding Personal Debt

Personal debt includes all forms of money owed, such as credit card balances, personal loans, student loans, and mortgages. Proper debt management involves paying off these liabilities without compromising your financial well-being. By developing a clear strategy, you can reduce stress and work toward financial freedom.

Assessing Your Financial Situation

Before you can manage your debts effectively, you need a clear understanding of your financial situation. Start by listing all your debts, including:

● The total amount owed

● Interest rates

● Minimum monthly payments

● Due dates

Once you have a complete picture, calculate your total debt-to-income ratio (DTI). A lower DTI ratio improves your financial standing and ability to qualify for loans with better terms.

Creating a Budget

A budget is a powerful tool that helps you allocate your income to cover essential expenses while ensuring that a portion goes toward debt repayment. To create a budget:

Track your income and expenses: Understand where your money is coming from and where it’s going.

Identify areas to cut back: Find unnecessary expenses that can be reduced or eliminated.

Set realistic goals: Allocate a specific portion of your monthly income to debt repayment while covering basic living costs.

Prioritizing Debt Payments

When managing multiple debts, it’s essential to prioritize payments. Two popular methods include:

1. Debt Snowball Method:

Pay off debts from smallest to largest. This method builds momentum as you eliminate smaller debts quickly, providing a psychological boost.

2. Debt Avalanche Method:

Focus on paying off debts with the highest interest rates first. This approach minimizes the total interest paid over time, making it more cost-effective.

Exploring Debt Consolidation Options

Debt consolidation involves combining multiple debts into a single loan with a lower interest rate. Common methods include:

● Personal loans: Take out a loan to pay off high-interest debts.

● Balance transfer credit cards: Transfer existing credit card balances to a card with a lower introductory interest rate.

● Home equity loans: Use the equity in your home to consolidate debts, but be aware of the risks involved.

Negotiating with Creditors

If you’re struggling to keep up with payments, consider negotiating with your creditors. Many lenders offer hardship programs, lower interest rates, or reduced payment plans if you explain your situation.

Avoiding New Debts

To successfully manage your existing debts, avoid accumulating new ones. This means:

● Limiting the use of credit cards

● Postponing major purchases until you can pay for them in cash

● Sticking to your budget and living within your means

Building an Emergency Fund

An emergency fund acts as a financial buffer, preventing you from relying on credit cards or loans during unexpected events. Aim to save at least 3 to 6 months’ worth of living expenses in a separate account.

Monitoring Your Progress

Debt management is a long-term process. Regularly monitor your progress by:

● Tracking your debt balance

● Reviewing your budget

● Celebrating small milestones

This will help keep you motivated and ensure you stay on track toward your debt-free goal.

Seeking Professional Help

If your debt becomes overwhelming, don’t hesitate to seek help from a financial advisor or a credit counseling agency. They can provide personalized advice and recommend solutions such as debt management plans (DMPs) or bankruptcy if necessary.

FAQ

1. How can I manage my credit card debt effectively?

You can manage credit card debt by creating a budget, paying more than the minimum, using the debt avalanche or snowball method, and avoiding new charges.

2. What is the best way to reduce high-interest debt?

The debt avalanche method is often the most effective, as it focuses on paying off debts with the highest interest rates first, minimizing the overall cost of borrowing.

3. Should I consider debt consolidation?

Debt consolidation can be a good option if you can secure a lower interest rate than your existing debts. However, it’s important to avoid taking on new debt after consolidation.

4. How do I negotiate with creditors?

Contact your creditors directly, explain your financial situation, and ask if they can offer a lower interest rate, reduced payment plan, or a temporary hardship program.

5. How long does it take to become debt-free?

The time it takes depends on the total debt amount, your repayment strategy, and your ability to stick to your plan. It can take anywhere from a few months to several years.

Thanks for taking the time to read Wealth Blueprint.

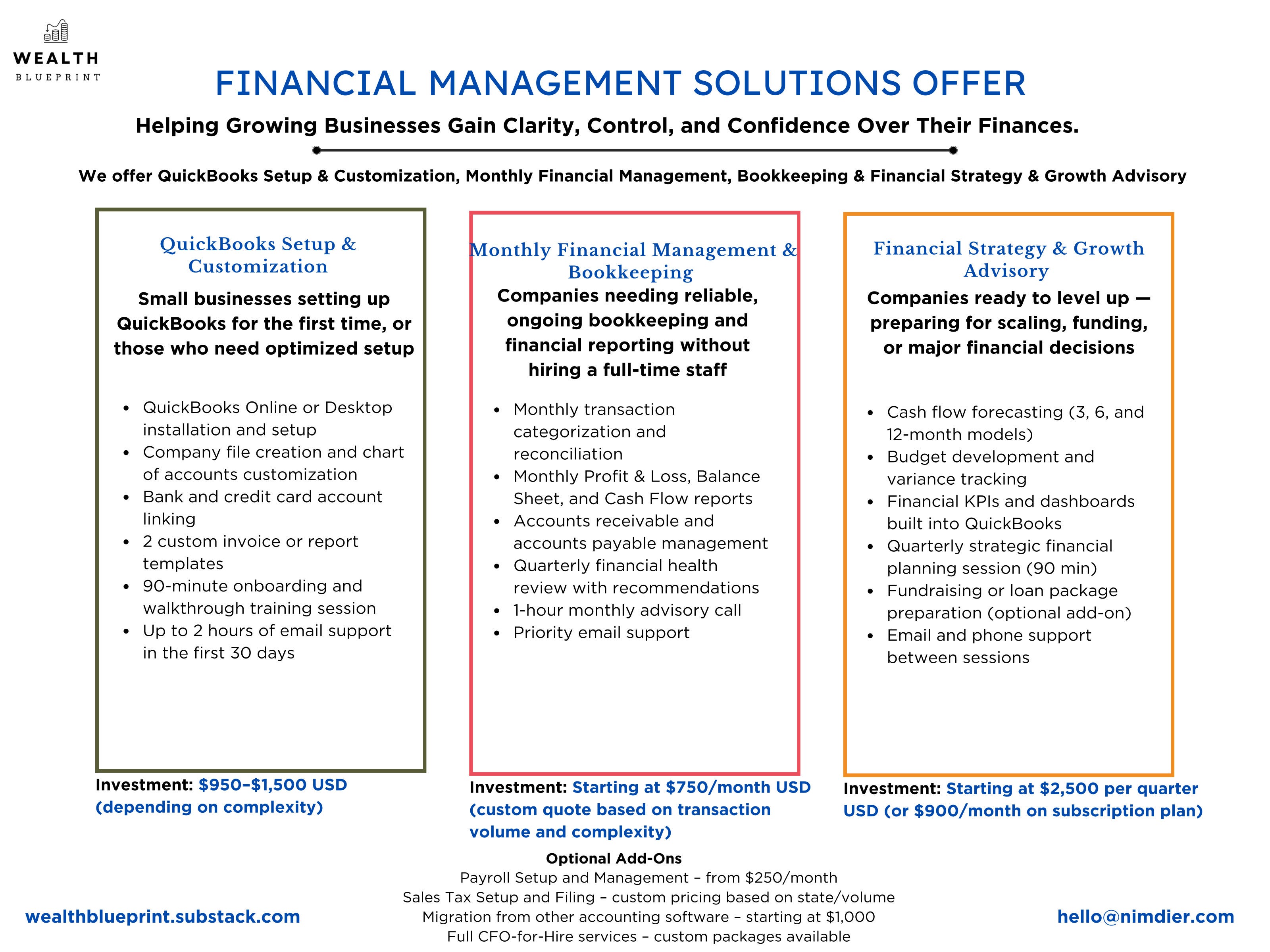

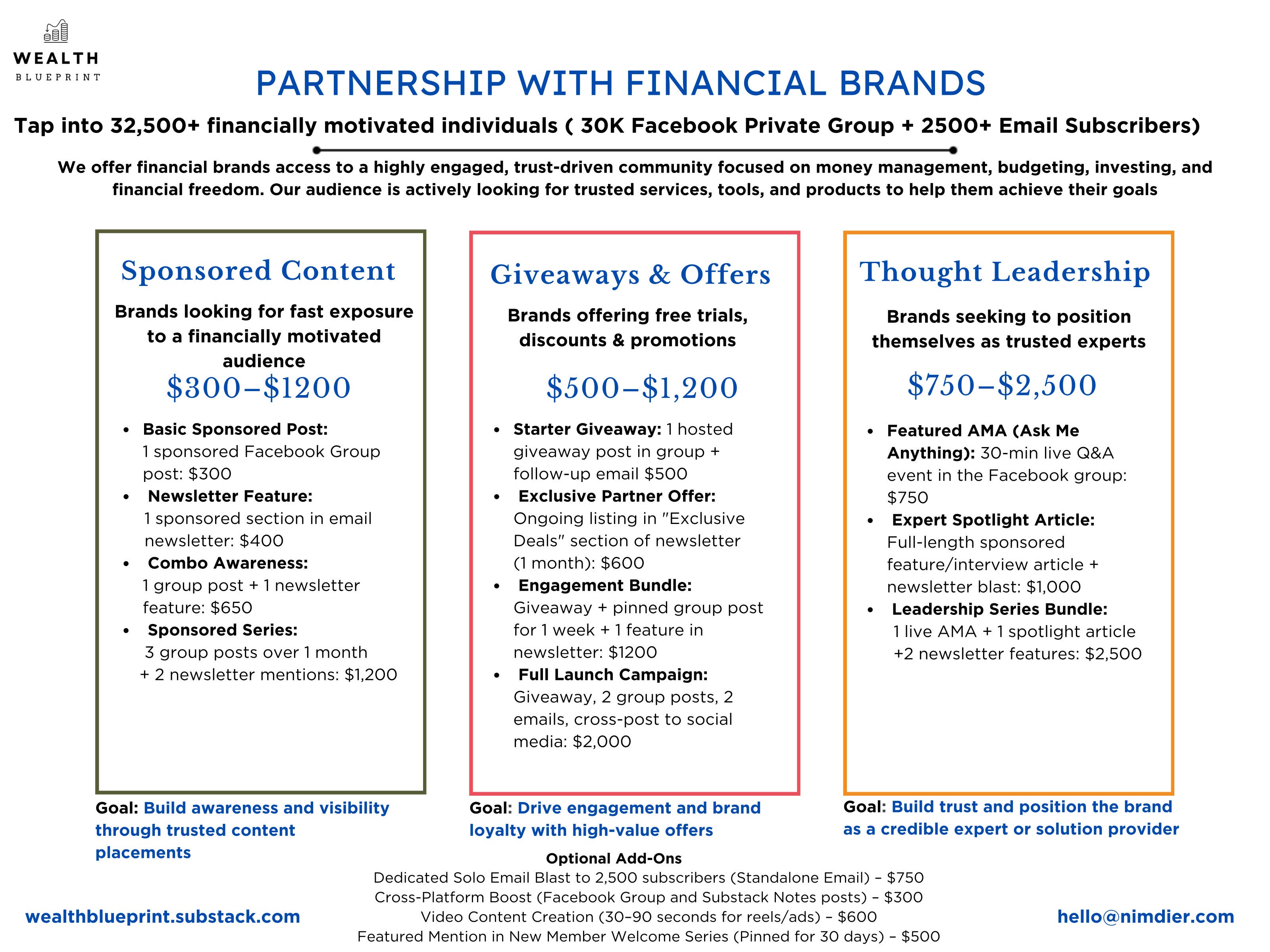

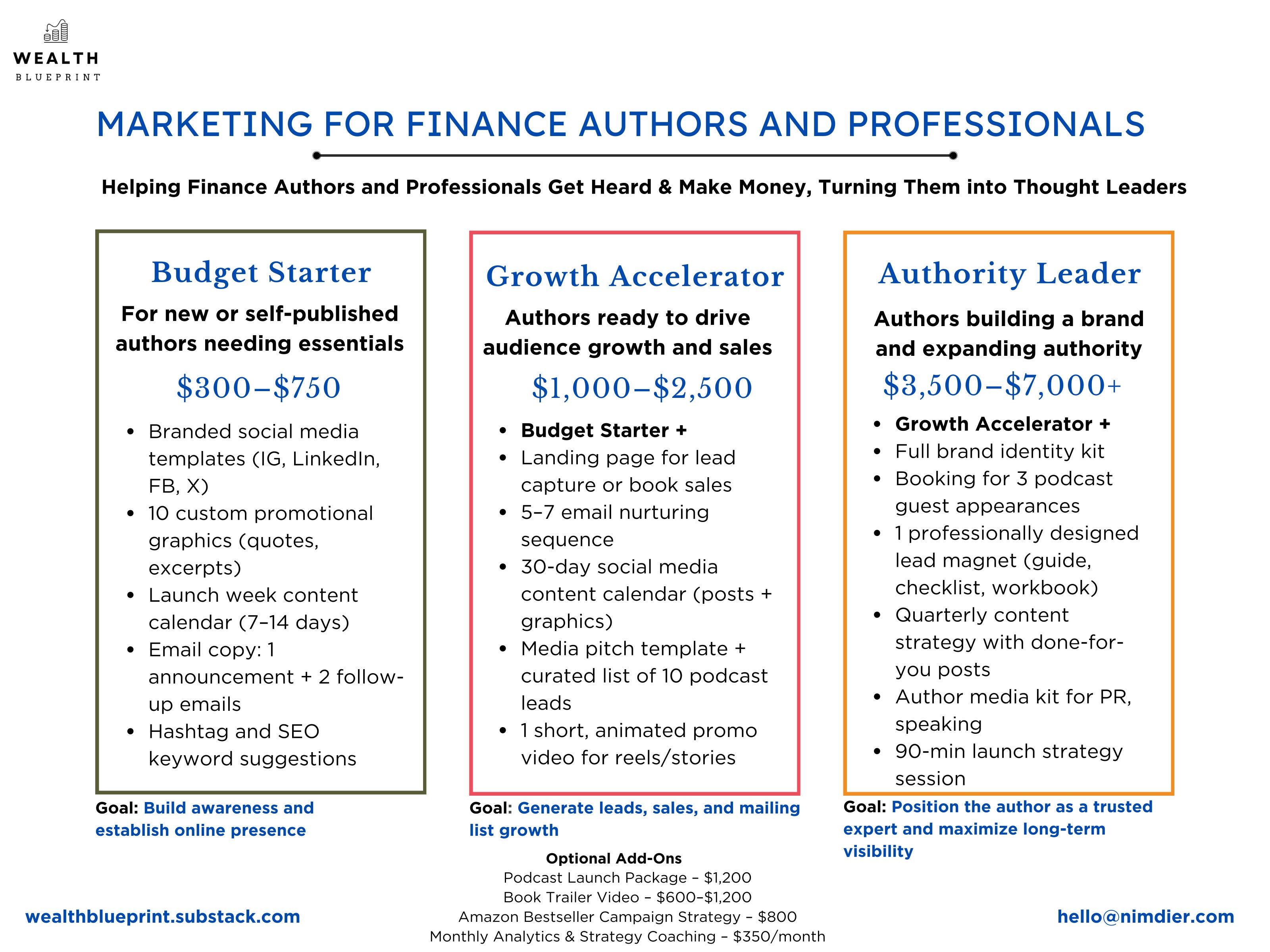

P.S. When you're ready, here are three ways we can help you manage your finances as a small or mid-size business. We also work with financial service brands and finance authors or professionals looking to grow their brands, book more business, and make more money.

Contact us at: hello@nimdier.com

OUR SERVICES: